- June 18, 2026

- Posted by: Tresmark

- Categories:

Most discussions of treasury function quality focus on operational efficiency: how quickly positions consolidate, how accurately cash is forecast, how smoothly payments process. These are legitimate measures. They are not the ones a CFO presents to the board or explains to investors when a working capital ratio underperforms, a borrowing cost sits above the peer benchmark, or an FX cost line represents a larger margin drag than the business’s currency exposure would suggest it should.

The financial outcomes.

For a CFO accountable for results that carry treasury roots, the operational quality of the treasury function matters primarily as a means to an end. A working capital position that reflects the business’s actual cash dynamics rather than the limitations of the data infrastructure tracking them. A borrowing cost that reflects the organization’s genuine liquidity position rather than the uncertainty premium of operating without current cash visibility. An FX cost outcome that reflects the currency exposure the business actually carries rather than what the last reporting cycle was able to measure. Each of these represents the same gap: the difference between the financial result the organization’s underlying position would support and the result its data infrastructure actually produces.

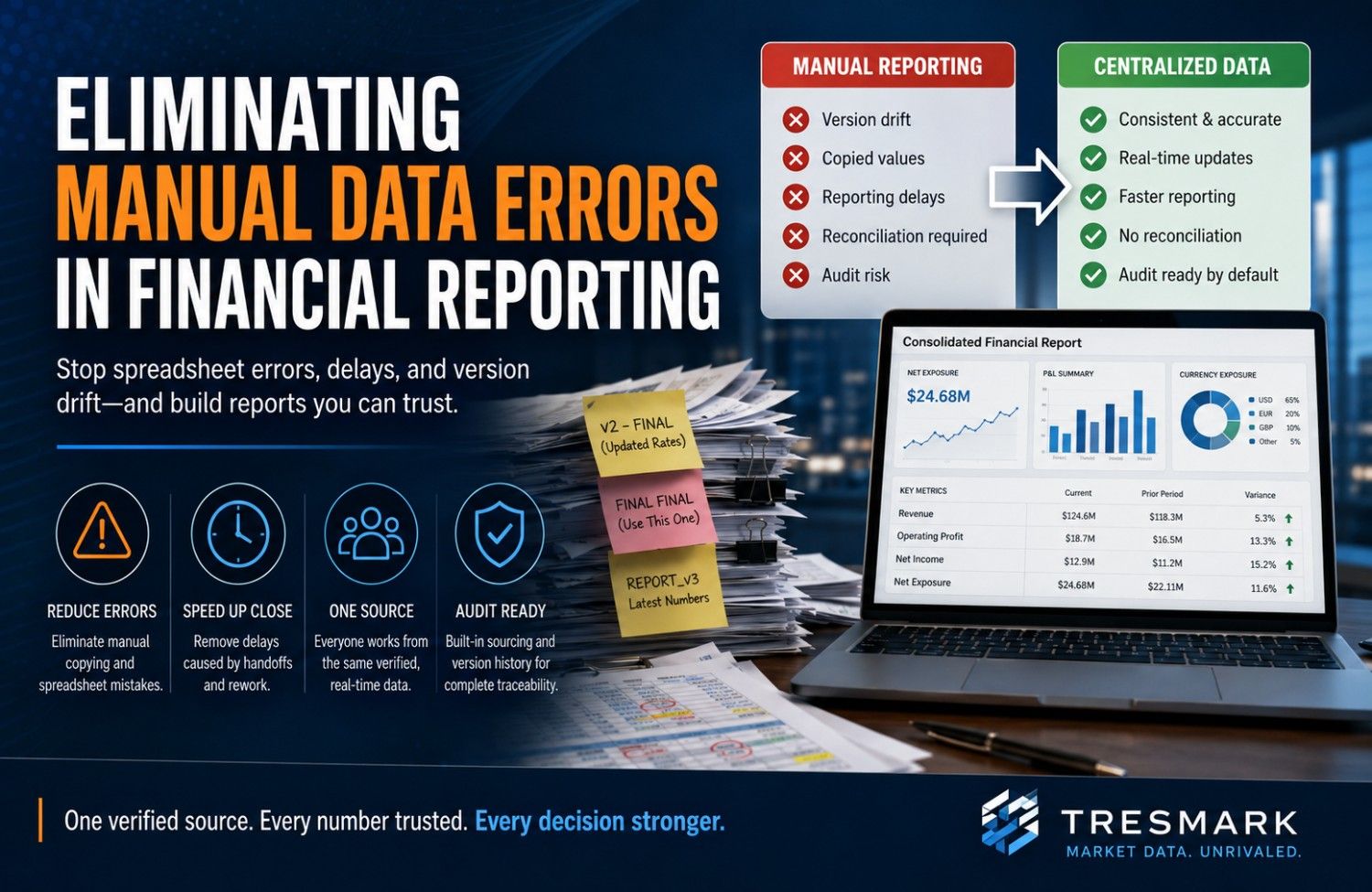

How Treasury Data Quality Affects Working Capital Performance

Cash conversion performance is where treasury operations connect most directly to financial results that appear in reporting and require explanation. The cycle itself, how quickly the business converts investments in inventory and receivables into cash, is sensitive to the quality and currency of the positioning data treasury uses to make payment timing and collection management decisions. When that data is accurate and current, working capital decisions reflect actual cash dynamics. When it is stale, fragmented, or assembled from systems that do not reconcile in real time, the decisions are made against a picture that may look acceptable while the underlying position has already shifted.

Payment scheduling is where data quality produces the most direct consequence. A treasury team with accurate, real-time cash visibility across entities can manage scheduling to optimize the conversion cycle, accelerating collections when liquidity is tighter than forecast, extending payment timing within agreed terms when cash availability supports it, identifying intercompany settlement opportunities that reduce external borrowing requirements. A team working from a consolidated position that is several hours old, assembled from banking portals updating on different schedules, makes the same decisions against conditions that no longer reflect current reality. The outcome is not dramatically wrong. It compounds across payment cycles and collection periods into a conversion cycle that runs consistently slower than actual cash dynamics would support. Treasury teams that optimize collection terms enhance cash flow reliability and reduce financing needs, with collection term management directly bearing on DSO and the speed of cash conversion.

Cash flow forecasting carries its own working capital consequence. Working capital management depends on visibility not just into current positions but into near-term flows: when receivables will clear, when payables fall due, when intercompany settlements will move. A treasury function producing forecasts from fragmented, delayed position data is building forward-looking decisions on a baseline that may already be inaccurate. The resulting forecast variance is not purely a forecasting quality problem. It reflects the data quality of the inputs behind the forecast, and that data quality has a direct consequence that appears in financial results as a conversion metric underperforming what the business’s operational conditions should produce. The data consolidation foundation that supports current working capital visibility is examined in how centralized data improves treasury efficiency.

Where FX Exposure Visibility Connects to Financial Results

Currency movements affect financial results through two distinct channels for businesses with international operations. The first is the translation effect: how currency moves change the reported value of foreign-denominated assets, liabilities, and earnings when consolidated into the reporting currency. The second is the transaction effect: the actual cash cost of settling foreign currency obligations at rates that differ from what was anticipated when the transaction was entered. Treasury’s influence over financial results runs primarily through the transaction channel, specifically through how accurately and currently the function can see its FX exposure across operating entities before coverage decisions are made.

Exposure accuracy sits at the root of most treasury-related FX cost underperformance. When a treasury team consolidates FX exposure from multiple entities reporting at different times in different formats, the aggregate picture used to assess coverage requirements reflects conditions from several points in time simultaneously rather than a single current moment. Without current treasury infrastructure, companies relying on delayed, manual processes to monitor FX exposure face earnings volatility from unhedged currency movements that erode margins, alongside cash flow mismatches where exchange rate shifts create timing gaps between receivables and payables that disrupt working capital cycles. The financial consequence is not primarily a catastrophic uncovered currency move. It is a persistent pattern of coverage decisions made against an exposure picture that was never fully current, producing FX costs above what accurate, consolidated data would have supported. The multi-entity FX exposure consolidation mechanics behind this picture are examined in the role of treasury in financial risk management.

Reactive coverage timing produces its own financial cost. An FX exposure identified and assessed only at the point where it requires coverage has fewer available approaches at a higher cost than one identified earlier in its lifecycle. When treasury can see developing exposures as they accumulate across entities, as transactions are entered, as intercompany obligations are created, as foreign currency receivables are recognized, the coverage assessment can happen at a point where the cost of managing the exposure is lower and the options wider. The financial consequence of reactive timing is an FX cost line reflecting market conditions at the point where coverage became unavoidable rather than the conditions available across the full period when coverage was possible. How the macroeconomic and currency signals that drive these outcomes can be monitored alongside commodity exposure is examined in what economic indicators are and how they affect markets. Kyriba describes FX risk management as critical for international operations, noting that managing currency fluctuation exposure directly mitigates its potential impact on financial performance and profitability.

How Liquidity Visibility Affects Borrowing Costs and Capital Efficiency

One of the most direct financial consequences of poor treasury data visibility is higher borrowing costs. This impact typically arises through two related mechanisms in multi-entity organizations: trapped cash and precautionary borrowing.

Trapped cash occurs when surplus funds are held within individual entities but are not visible as available liquidity at the group level. As a result, one business unit may maintain excess cash balances while another draws on external credit facilities to meet short-term funding needs. Without a consolidated, real-time view of liquidity across the organization, treasury teams cannot efficiently deploy available cash to offset borrowing requirements.

Precautionary borrowing occurs when treasury teams draw on credit facilities earlier than necessary because liquidity forecasts are based on incomplete or delayed information. When cash positions, receivables, and funding requirements are not visible in real time, uncertainty increases. To avoid the risk of a shortfall, organizations maintain larger liquidity buffers and borrow more conservatively than actual cash conditions require.

Organizational complexity amplifies both challenges. A multinational business may hold significant cash balances across regional subsidiaries while simultaneously utilizing a revolving credit facility at the group level. The cash is visible within local reporting structures but does not function as available liquidity unless treasury has a consolidated view of positions across all entities. According to PwC’s 2025 Global Treasury Survey, leading treasury organizations are increasingly using real-time liquidity tools and centralized treasury structures to improve cash efficiency and reduce reliance on external funding.

The result is a hidden cost of fragmented liquidity visibility. Borrowing costs become higher than they need to be, not because of credit risk or funding constraints, but because treasury teams lack a complete picture of available cash resources.

Three common consequences include:

- Higher borrowing costs from trapped cash: External borrowing continues while surplus cash remains idle elsewhere in the organization, creating avoidable interest expense.

- Excess facility utilization: Forecast uncertainty leads to larger and earlier credit facility drawdowns than actual liquidity requirements justify.

- Reduced cash concentration efficiency: Cash pooling and liquidity optimization decisions are made using incomplete information, limiting the effectiveness of group-wide treasury management.

The governance implications of these visibility gaps are explored further in our article, How CFOs Can Gain Better Control Over Treasury Functions.

How the between-cycle visibility gap that produces these blind spots appears from the CFO’s governance perspective is examined in how CFOs can gain better control over treasury functions.

Why Treasury’s Financial Contribution Is Difficult to Measure and Easier to Miss

When the treasury function is performing well, its contribution to financial results is invisible. Working capital conversion runs at the right level. FX costs sit within acceptable variance. Borrowing costs reflect the organization’s genuine credit profile rather than a data quality premium. The contribution of data infrastructure quality to those outcomes is present in the results but cannot be isolated, attributed, or demonstrated from them alone. The connection only becomes traceable when something goes wrong.

That traceability gap creates a specific organizational challenge. The investment case for better treasury data infrastructure is most compelling in organizations that have already experienced a treasury-related financial performance problem: a working capital deterioration traced to cash positioning inaccuracy, a borrowing cost running above peer benchmarks for reasons that eventually traced back to trapped cash the function could not see, an FX cost overrun reflecting reactive coverage timing rather than the business’s underlying currency exposure. In organizations where those problems have not yet surfaced, the case depends on articulating a financial risk that has not yet materialized rather than a cost already in results. That is a harder argument to make to a board looking at acceptable current performance rather than the gap that current data infrastructure is quietly producing. How the decision confidence that real-time visibility creates at the leadership level changes this organizational dynamic is examined in how real-time visibility helps leadership make better financial decisions.

Demonstrating treasury’s financial contribution requires connecting specific operational data quality metrics to specific financial outcomes in a way most treasury functions currently cannot do. A treasury team that can show the relationship between cash positioning accuracy and DSO performance, between liquidity forecast variance and external facility utilization, between FX exposure consolidation timeliness and FX cost outcomes, is making a financial performance case that goes beyond operational efficiency metrics. It is showing the CFO and board that data infrastructure quality has a measurable effect on the financial results they are accountable for, not just on how smoothly the function runs. How forecasting accuracy as a specific financial performance metric connects treasury operational quality to planning outcomes is examined in how financial data platforms support better forecasting.

Treasury Data Quality as a Financial Performance Variable

Working capital metrics, FX cost outcomes, and borrowing costs are not purely a function of market conditions or business model characteristics. Each carries a data infrastructure dimension that determines how closely the financial result reflects the organization’s underlying position. The gap between the result the organization’s actual position would support and the result its data infrastructure produces is where treasury’s connection to financial performance sits most precisely and where the investment case for better treasury data is most clearly grounded.

Making that case in financial terms changes how treasury infrastructure decisions are evaluated. How many basis points of borrowing cost does current, consolidated liquidity visibility remove from the cost of debt? How many days of cash conversion cycle improvement does accurate, real-time cash positioning enable? What reduction in FX cost line variance does current, consolidated exposure data produce? These are measurable financial outcomes. They belong in the investment case alongside the operational efficiency arguments, and they make a more compelling case to a CFO and board evaluating treasury infrastructure than workflow improvement metrics alone.

Treasury data quality delivers four specific financial performance outcomes:

- Working capital improvement: current, consolidated cash positioning enables payment timing and collection management that reflects actual operating conditions rather than fragmented, delayed data, producing a conversion cycle running closer to what the business’s cash dynamics support

- FX cost reduction: current FX exposure data across entities supports coverage assessment against an accurate, consolidated picture rather than one assembled from multiple reporting cycles, reducing the FX cost premium that inaccurate exposure data produces

- Borrowing cost reduction: real-time liquidity visibility across entities surfaces idle cash that offsets external borrowing requirements and reduces precautionary facility utilization, lowering the cost of debt toward what the organization’s genuine liquidity position would support

- Financial performance traceability: connecting treasury operational data quality metrics to specific financial outcomes gives finance leadership the ability to demonstrate treasury’s contribution before problems surface rather than only after they appear in results

Treasury functions operating with current, connected data infrastructure produce outcomes that more accurately reflect the financial position the business actually holds. The data quality premium that inadequate infrastructure adds to borrowing costs, working capital cycles, and FX cost lines is not a market condition. It is a measurable, addressable gap between the financial results the organization’s position supports and the results its data infrastructure delivers.

Tresmark’s treasury market data and visibility platform gives treasury teams and finance leadership real-time visibility across cash positions, FX exposure, liquidity data, and market rates, providing the connected data environment that treasury financial performance management requires.