- January 2, 2026

- Posted by: Tresmark

- Categories:

T-bills attract $20m in net foreign inflows

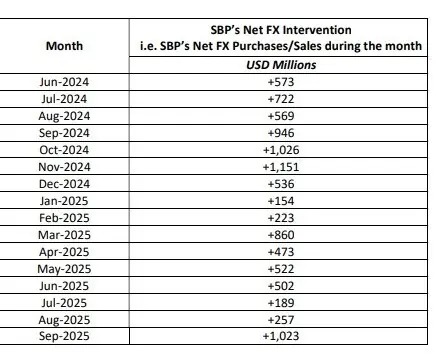

Pakistan’s short-term local government bonds saw net foreign inflows of $20 million in December, compared with $42.2 million in outflows recorded in the previous month.Overseas investors poured $77.29 million in treasury bills as of December 25 but divested $57.27 million, data from the State Bank of Pakistan showed on Thursday.

Analysts said that foreign investment in T-bills fluctuated significantly in 2025. There were outflows during the first half of the year due to geopolitical uncertainties and high yields in other countries. Additionally, the reduction in interest rates in Pakistan diminished foreign appetite for local bills and bonds. However, in the second half of the year, foreign investment in T-bills began to stabilise, and the turnaround in December indicates renewed foreign interest as Pakistan’s risk premium decreases and policy continuity improves.

The SBP unexpectedly cut its benchmark interest rate by 50 basis points to 10.5 percent in December. It had kept interest rates unchanged at 11 percent for four straight policy meetings before December 15. The central bank last cut rates in May 2025. With the latest reduction, the SBP’s Monetary Policy Committee (MPC) has lowered rates by 1,150 basis points since they peaked at 22 percent in June 2024.

The Only Financial Information Platform You Need

Tresmark is the market leader, the only tool you need for a full picture od the financial markets

Over the past two years, Pakistan’s sovereign narrative has shifted from acute default fears to a gradual restoration of market confidence, underpinned by rating upgrades from Moody’s and Fitch reflecting stronger policy discipline, improved external buffers, better liquidity management, and progress under the International Monetary Fund’s loan programme, said Ismail Iqbal Securities in a report published last month. “This turnaround is evident in a sharp rally in Pakistan’s Eurobonds across maturities, signalling a broad reassessment of sovereign

risk, supported by higher reserves, a narrowing current account deficit, and repayment of select short-term liabilities,” the report said.“Looking ahead, plans to reenter capital markets starting with a potential Panda bond in CY26 and a broader return to Eurobond and Global Sukuk issuance by FY27 reflect renewed policy credibility and improved funding flexibility, marking a decisive shift away from crisis pricing toward a more stable and investable sovereign outlook,” it added.