- January 2, 2026

- Posted by: Tresmark

- Categories:

Why the Rupee Was Never the Real Problem

Who remembers 1998, when Pakistan’s currency market broke down?

The trigger was nuclear testing and the sudden pullback of external financing. The foreign exchange (FX) market melted down, confidence evaporated, and multiple exchange rates emerged. One could call it a black swan event.

But Pakistan’s FX crises did not end there.

If we examine the major episodes that followed in 2008, 2018, and 2022 a clear and repeatable pattern emerges. What actually triggered these crises was not the currency itself, but a combination of political instability, policy paralysis, oil price shocks, inflation surges, geopolitical disruptions, and breakdowns in International Monetary Fund (IMF) programmes.

In each case, the initial shock originated outside the FX market. The rupee was not the cause; it became the transmission channel. Once these shocks hit, they exposed pre-existing vulnerabilities: elevated inflation, wide current account deficits, weak reserve buffers, delayed interest rate adjustments, and, critically, the absence of credible IMF anchors.

When Stress Turned Into Crisis: The Role of Sentiment

Exposure alone did not create a crisis. What followed determined the outcome.

The turning point in every episode was a shift in sentiment. As confidence weakened, capital flows slowed and expectations changed abruptly. At this stage, the rupee’s behaviour became sentiment-driven rather than valuation-driven.

Policy responses then became decisive and historically, they followed a familiar but damaging path. Instead of allowing early adjustment, authorities attempted to defend the rupee, burned through reserves, and delayed decisive action.

This combination transformed manageable stress into full-blown crisis. Speculative hoarding intensified, and by the time adjustment finally occurred, it was forced, disorderly, and credibility-destroying. This is why Pakistan’s FX history is characterised by sharp step devaluations rather than smooth, gradual depreciation.

A Structural Shift: The Current SBP Regime

Under the current State Bank of Pakistan (SBP) regime, supported by the IMF, the framework for macroeconomic management has shifted meaningfully.

The rupee remains an important optic, but reserves now anchor policy credibility.

This implies three critical changes:

- The exchange rate is allowed to move in both directions, rather than being held at an artificial level.

- SBP intervention focuses on smoothing volatility, not defending the rupee at the cost of reserves.

- Periods of FX strength are used to rebuild buffers, not to signal short-term stability.

This regime materially lowers the probability of a repeat of past devaluation episodes. However, it also caps upside. The objective is not a stronger rupee at any cost, but a more resilient external position anchored by reserve strength.

In this framework, reserves absorb shocks, remittances provide durable support to the external account, and import compression manages excess demand. Short-term administrative measures — the so-called “danda” — are used to curb hoarding and speculative pressure when necessary.

Volatility may still occur, but with adequate reserves, it becomes reversible rather than destabilising.

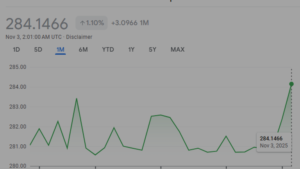

What Comes Next: Rupee Dynamics Into 2026

Looking ahead, rupee dynamics will be driven less by valuation gaps and more by a small set of structural forces:

- Inflation and interest rate differentials

- Political continuity and policy credibility

- External financing capacity and fiscal discipline

- Reserve accumulation behaviour

Meanwhile, the trade balance will remain sensitive to oil prices, regional export competitiveness, geopolitical developments, and global recession risk.

So how might the rupee perform into 2026?

Scenario Analysis:-

Bear Case: Early Adjustment, Not Crisis

This scenario reflects political disruption, fiscal slippage, or renewed stress with the IMF. Inflation pressures re-emerge, and reserve accumulation stalls.

The rupee weakens more sharply. However, unlike past episodes, adjustment occurs earlier. The central bank does not exhaust reserves defending the currency. Administrative measures are deployed to manage speculation, while import compression reduces demand.

With a flexible exchange rate and a clear focus on preserving reserves, step devaluations become far less likely — even under stress.

Base Case: Inflation Defines the Drift

Over the medium term, the rupee broadly follows inflation differentials. Pakistan’s inflation trend remains meaningfully higher than that of the United States. Even with gradual disinflation, the gap is likely to hover around five percent.

This implies a steady, orderly depreciation rather than a sharp or disorderly adjustment. In this scenario, the rupee weakens gradually without triggering stress in reserves or confidence — the outcome markets are most comfortable with.

Bull Case: Stability With Buffers

This scenario assumes political continuity, an intact IMF framework, and a stable geopolitical environment. Fiscal discipline holds, external financing remains available, and bond and multilateral inflows support faster reserve accumulation.

In this environment, the rupee may trade firmer for extended periods. However, upside remains capped by reserve accumulation objectives and export competitiveness. Stability improves, but growth remains secondary. Given current trends, this appears to be the most likely near-term scenario.

The Only Financial Information Platform You Need

Tresmark is the market leader, the only tool you need for a full picture od the financial markets

About the Author:-

Faisal Mamsa is the CEO of Tresmark, a financial market data and analytics platform. He writes on macroeconomics, currency markets, and policy credibility in Pakistan.

Publication Note

This article was originally published in Dawn – The Business and Finance Weekly on December 29, 2025. It is republished on Tresmark’s website for reference and wider access

r0fy1p